SMM1 March 15: throughout 2020, affected by the global epidemic in the first half of the year, the new energy industry entered a downturn, but with the improvement of the domestic epidemic and the opening of consumer market demand, Tesla's "catfish effect" brought a continuous increase in the number of new models of new energy vehicles, improved battery performance and mileage, and the gradual improvement of charging facilities. The new energy market quickly picked up in the second half of the year, and the industry rekindled confidence in China's new energy market. The SMM new energy analysis team investigates and integrates the production data of China's core battery materials, summarizes the characteristics of the price trend, makes an annual review and summary of the new energy battery material market in 2020, and makes a judgment and forecast of the price trend in 2021.

This is the third of a series of analysis reports, which describes the conclusions and forecasts of the core data of the positive industry:

In 2020, China's total output of ternary materials was 215000 tons, an increase of 10.5% over the same period last year. SMM expects the output of ternary materials to be 295000 tons in 2021, up 37.1% from the same period last year.

In 2020, China's total output of lithium iron phosphate was 147000 tons, an increase of 61.2 percent over the same period last year. SMM expects lithium iron phosphate production to be 240000 tons in 2021, up 63.3% from the same period last year.

In 2020, China's total output of lithium manganate was 58000 tons, an increase of 7.7 percent over the same period last year. SMM expects lithium manganate production to be 70, 000 tons in 2021, a year-on-year increase of 21%.

In 2020, China's total output of lithium cobalt was 75100 tons, up 22% from the same period last year. SMM expects lithium cobalt production to be 79000 tons in 2021, an increase of 5.2 per cent year-on-year.

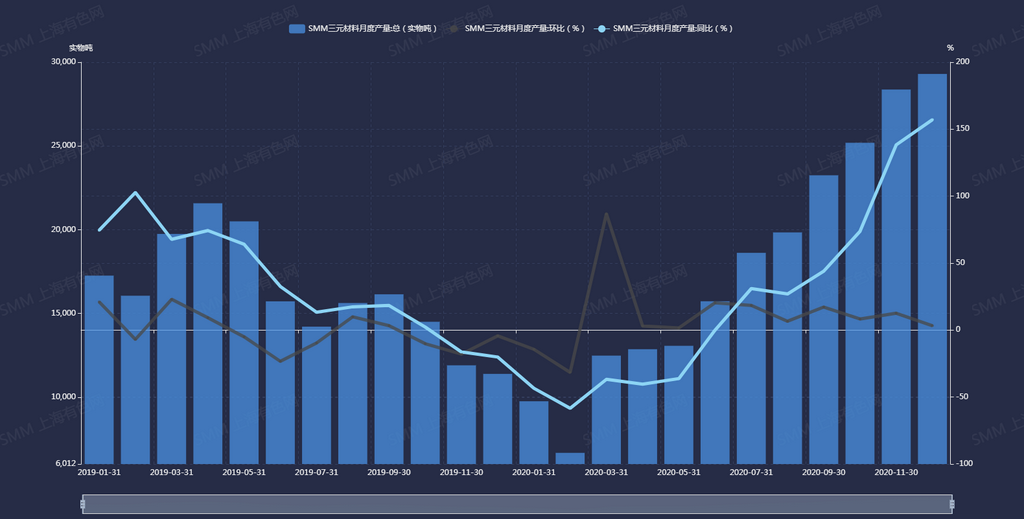

Output of ternary materials in China from January 2019 to December 2020

Source: SMM

In 2020, China's total output of ternary materials was 215000 tons, an increase of 10.5% over the same period last year. Affected by the epidemic in the first half of the year, the market operating rate was relatively low in the first quarter, and production dropped seriously compared with the same period last year In the second quarter, ternary material enterprises basically resumed operation, but the downstream consumer market has not yet recovered, and the output is still low. In the second half of the year, with the recovery of the new energy market, the output of ternary materials increased month by month. In the fourth quarter, the market of new energy vehicles was hot, year-end rush and strong consumer demand, power demand increased sharply, and the output of ternary materials increased significantly. Among them, only the output from September to December exceeded 20,000 tons, and the annual output showed the characteristics of low and half a year high in the first half of the year.

Car companies have gradually digested the decline of subsidies for new energy vehicles, coupled with new energy activities to the countryside and the listing of the low-end model Hongguang MINI, the low-end market demand that does not rely on subsidies has increased significantly. In addition, best-selling models such as Tesla Model 3, Guangzhou Automobile AION S, Xilai EC6, Xiaopeng P7 and ideal ONE also bring greater demand for the Sanyuan market. In the whole year, five enterprises produced more than 15000 tons, with a CR10 of 70% and a CR5 of 44.8%. In December 2020, China's total output of ternary materials was 29000 tons, up 157.1% from the same period last year and 3.3% from the previous month, the largest monthly increase since 2020.

The total production capacity of ternary materials has reached 608000 tons in 2020, an increase of 230000 tons compared with 2019, with obvious overcapacity and fierce market competition. at the same time, large manufacturers of Sanyuan materials are also gradually bound to downstream head battery enterprises, and the customer structure is relatively concentrated. once downstream battery customers increase or reduce production on a large scale, if the upstream raw material production plan is not adjusted in time, there will be a shortage of supply or a large accumulation of inventory.

According to SMM, Tesla Model Y and Volkswagen ID.4 are listed in 2021. In addition, many big battery manufacturers have signed cooperation agreements with overseas car companies. SMM expects that the entry of foreign car companies and the increase in overseas markets will drive the domestic demand for 8-series ternary materials, so the output of high-nickel ternary materials will increase, while the output of 5 and 6 series ternary materials will increase slightly. The annual output of ternary materials in 2021 is expected to be 295000 tons. A year-on-year increase of 37.1%.

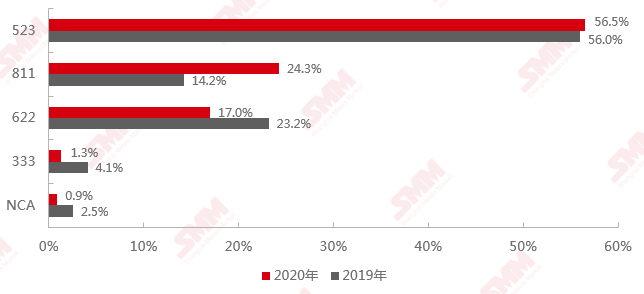

Comparison of product structure of ternary materials in China in 2020 and 2019

Source: SMM

From the point of view of yield structure, the trend of high nickelization is still obvious. In 2020, the proportion of ternary materials 523 is 56%, which is basically unchanged compared with 2018; 622 is 17%, which is 6.2% lower than that in 2018; and the proportion of high nickel 811 is 24.3%, which is much higher than that in 2019.

Due to the frequent safety accidents of high-nickel models this summer, the market demand for high-nickel ternary has weakened, coupled with the optimization of battery package structure this year, 5-series ternary + CTP technology has been gradually used in new models, the domestic 5-series ternary output has increased, the domestic 8-series demand is stable, and the increment basically comes from abroad. SMM predicts that in order to meet the mileage demand of electric vehicles in the future, high nickel is the only way for the development of ternary materials. In the future, with the development of star high-end models and the development and safety of high-nickel batteries in battery factories, the output of low-and medium-nickel ternary materials may further decline.

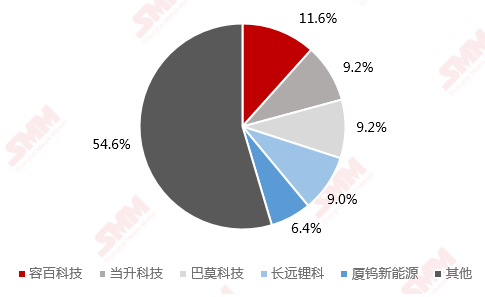

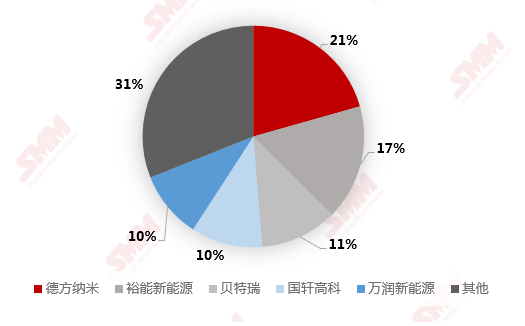

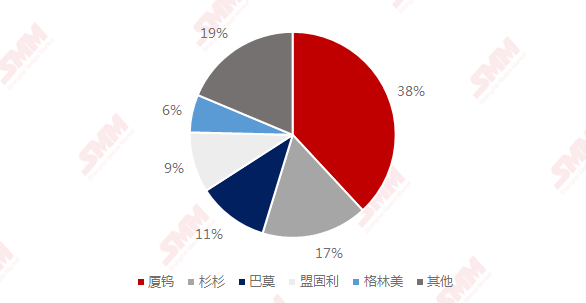

Top five market share of ternary material manufacturers in 2020

Source: SMM

The market share of ternary material Top 5 has reached 44.8%. Now the industrial concentration is slightly higher than in 2019. Large factories actively expand production after stable cooperation with downstream power battery factories, while small and medium-sized factories can only rely on small power and digital market, facing the problem of overcapacity. According to SMM, there are many new capacity planning enterprises from 2021 to 2023, such as Huayou Cobalt, Hunan Shanshan, Xiamen Tungsten, Yibin Libao, Jingmen Greenmei, Dangsheng Technology, Guoxuan Hi-Tech, Hunan Bangpu, Hunan long-term, Ningbo Rongbai, Sichuan New Lithium want and other enterprises have expansion plans. As the current capacity utilization rate of the ternary material industry is less than half, the trend of product customization is significant, and the gross profit level varies greatly, SMM expects that only part of the downstream enterprises with good cooperative relations, joint ventures or enterprises with upstream raw material advantages have certain practical significance, and the production capacity of ternary materials in China will reach 1.05 million tons by 2023.

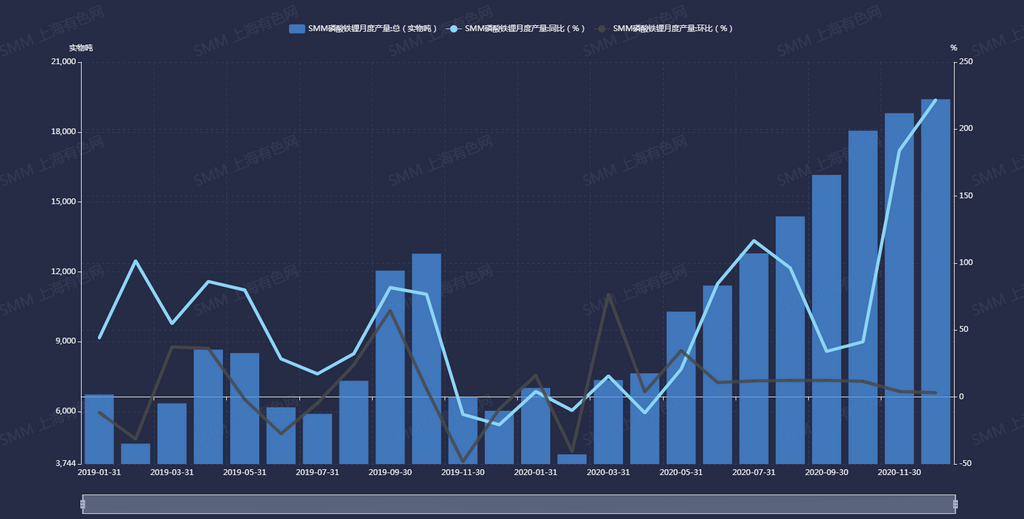

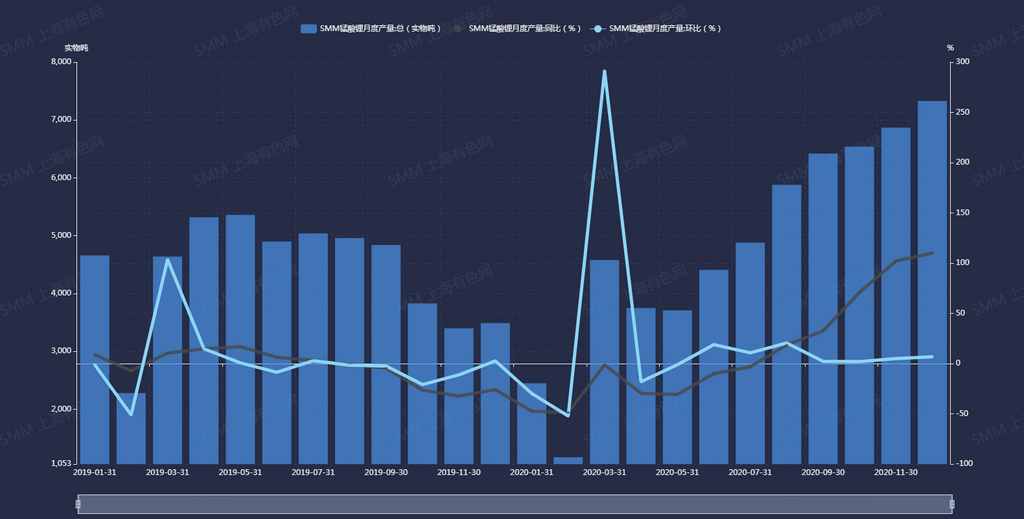

Output of Lithium Iron Phosphate in China from January 2019 to December 2020

Source: SMM

In 2020, China's total output of lithium iron phosphate was 147000 tons, an increase of 61.2 percent over the same period last year. In the whole year, six enterprises produced more than 10000 tons of lithium iron phosphate, with a CR10 of 92.4% and a precinct CR5 of 68.2%. In December 2020, China's total output of lithium iron phosphate was 19000 tons, up 221.9% from the same period last year and 3.2% from the previous month.

Affected by the epidemic after the Spring Festival, iron and lithium enterprises return to work slowly, some enterprises only officially resume production in March, and the operating rate is also relatively low after the start of work. In the second quarter, the national production of lithium iron phosphate returned to normal, due to the slow recovery of the power market, the opening of energy storage market orders, the slow growth of iron and lithium production, the high inventory of head battery enterprises, the operating rate of large factories is still not high, and the output of small and medium-sized enterprises is rare. In the third quarter, with the number of iron-lithium matching models in the power market, energy storage orders increased steadily, and the output of lithium iron phosphate increased month by month, of which the output in September exceeded 15000 tons for the first time. In the fourth quarter, the demand for iron and lithium power reached its peak, and the market demand for small power and energy storage was stable. Many large iron and lithium factories were close to full production and were in short supply, while small and medium-sized enterprises had fewer power orders and a slight increase in output.

With the emergence of blade battery and CTP technology, automobile companies pay attention to the energy density, safety and performance-price ratio of iron-lithium battery, and the supporting iron-lithium models are gradually increasing. In addition to occupying the low-end market of A00 and A0, iron-lithium also gradually leaps forward to the high-end market, iron-lithium in the power market demand gradually catch up with three yuan. In addition, the demand for iron lithium in domestic 5G base stations and overseas photovoltaic wind energy storage continues to increase, as well as the demand for iron lithium in electric two-wheeler market, heavy trucks, ships and other segments. SMM expects lithium iron phosphate production to be 240000 tons in 2021, up 63.3% from the same period last year.

Top five market share of lithium iron phosphate producers in 2020

Source: SMM

The market concentration of iron lithium remains high in 2020, and many small factories have gradually withdrawn from the market. German nano-customer group is better, involving more downstream areas, ranking first in 2020. In 2020, China will have a production capacity of 320000 tons of lithium iron phosphate, an increase of 78000 tons over 2019. The new production capacity in 2020 mainly comes from German Nano, Xiangtan electrification and Chongqing Teri. Many manufacturers cooperate with downstream head battery factories to increase production capacity, such as German Nano and Ningde era cooperation, new production capacity of 20,000 tons has been put into production. Although the trend of the iron-lithium market is better, the profit margin of the iron-lithium industry is low, even large factories have losses, and the market concentration is gradually increasing. at present, only large factories have plans to expand production in the future, and there are still many uncertainties in small and medium-sized factories. SMM expects that the growth rate of iron-lithium production capacity in the future is relatively low, and the ranking of the top five output may also change.

Output of lithium manganate in China from January 2019 to December 2020

Source: SMM

From January to December 2020, China's total output of lithium manganate was 58000 tons (excluding Xinxiang Hongli), an increase of 7.7% over the same period last year. The CR10 is 65.1% and the core CR5 is 36%. Due to the impact of the epidemic in China in the first quarter, lithium manganate enterprises often delay the resumption of production after the festival, and the operating rate is low. The global epidemic broke out in the second quarter, the export of end consumer goods was blocked, and the output of lithium manganate fell by nearly 30% year on year. With the improvement of the global epidemic in the second half of the year and the recovery of consumer market demand until the end of the year, coupled with the increasing demand for lithium manganate for electric two-wheelers, the output of lithium manganate increased by 20% and 30% compared with

SMM believes that with the further increase in market demand for small power such as electric bicycles in 2021, the popularity of new energy vehicles in the field of special-purpose vehicles, and the gradual increase in new consumer goods, the demand for lithium manganate materials may be boosted. SMM expects China's lithium manganate production to reach 70, 000 tons in 2021, up 21% from the same period last year.

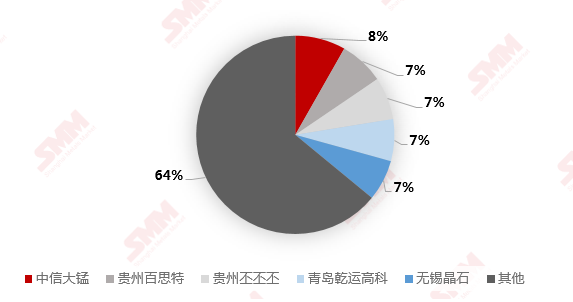

Top five market share of lithium manganate producers in 2020 (excluding Xinxiang Hongli)

Source: SMM

Due to the weak industry barriers, easy market entry, small mainstream manufacturers and scattered downstream demand, lithium manganate is involved in consumer, power and small power categories, but the overall demand is not high. There are more lithium manganate producers, the industrial concentration is lower than other cathode materials, and the annual concentration has not increased. The market share of Top 5 is 36%, the market competition is fierce, the bargaining power is weak, and the price is low for a long time.

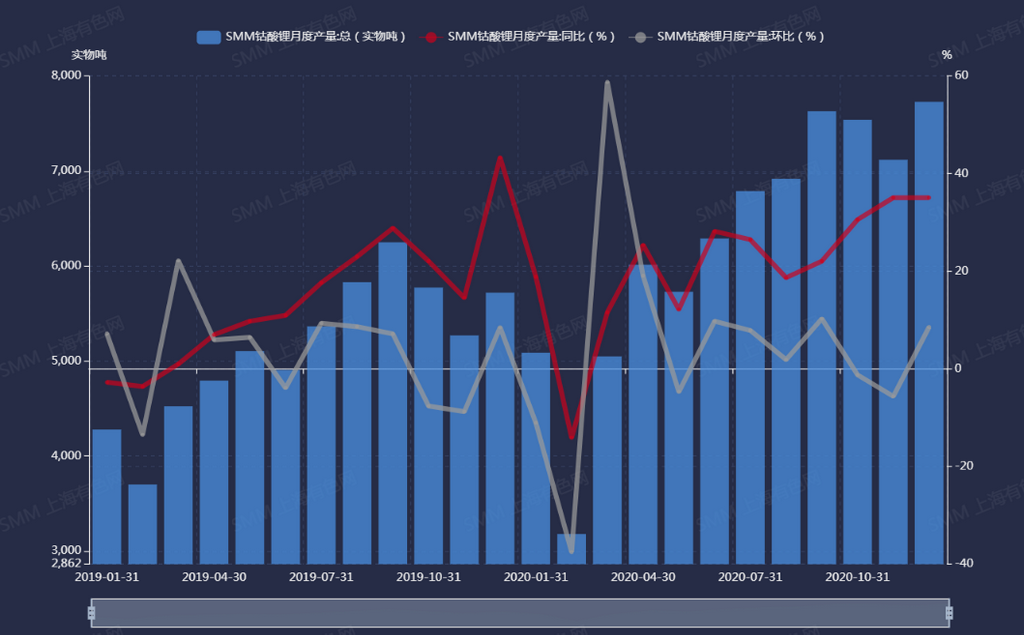

Output of Lithium Cobalt oxide in China from January 2019 to December 2020

Source: SMM

In 2020, China's total output of lithium cobalt was 75100 tons, up 22% from the same period last year. The domestic lithium cobalt industry is highly concentrated, with a CR5 of 81.3% in 2020. The market share of TOP5, a Chinese lithium cobalt manufacturer, decreased slightly by 0.64% in 2020 compared with 2019, and the market concentration is basically stable. Among them, the output of lithium cobalt in Xiamen Tungsten and Menggu Li in 2020 increased by 46.7% and 27.1% respectively compared with the same period in 2019.

TOP5 Market share of Chinese Lithium Cobalt oxide manufacturer in 2020

Source: SMM

Lithium cobalt material and battery industry chain is mature, because it is mainly used in the traditional 3C field, with the formation of downstream customer oligopoly market, the concentration of material factories is also very high, and the change of monthly output is mainly affected by the periodic changes of the industry.

In 2020, the output of Fujian, Beijing, Tianjin and Guangdong increased, while that of Hubei and Guizhou shrank. The annual output increased in the second and third quarters and decreased in the first and fourth quarters, which was consistent with the downstream demand cycle. This year, except for the domestic production decreased due to the epidemic in February, the supply of lithium cobalt oxide in the whole market increased in other months compared with the same period last year. It is expected that the demand for replacement machines will be driven by 5G in the future, and TWS headphones and other smart homes will also boost demand to a certain extent, which will affect the order of lithium cobalt oxide in 2021 or continue to grow. SMM expects lithium cobalt to produce 79000 tons in 2021, an increase of 5.2 per cent year-on-year.

Summary of key news of cathode material industry in 2020

On January 31, 2020, Greenwich and ECOPROBM signed a memorandum of understanding ((MOU)) on the procurement and cooperation of NCM8 series and 9 series high nickel precursor materials for new energy power batteries. From 2020 to 2026, ECOPROBM will purchase from the company a total of not less than 100000 tons of high-nickel NCM8 series and 9 series precursors, subject to the annual procurement contract.

2. On March 27, Huahai New Energy, a subsidiary of Huayou Cobalt, signed a "long-term purchase and sales contract for N65 precursors" with Posco. The total duration of the contract is 34 months, and the total quantity of products under the contract is about 76250 tons from March 2020 to December 2022. According to the contract estimated at the current market price, the total estimated contract amount is about 72-7.6 billion yuan, accounting for 38.19% of the company's audited operating income in 2019. 40.31%.

3. On April 28, after the completion of the long-term lithium battery cathode material expansion project, it will have an annual production capacity of 80,000 tons of power battery ternary materials. The construction of the project is committed to building a leading enterprise of battery cathode materials, which is expected to achieve a business income of about 12 billion yuan and a total annual profit and tax of about 600 million yuan. Hunan long Like Co., Ltd. vehicle lithium battery cathode materials expansion project is committed to the R & D and production of NCM and NCA products. The project is located in Changsha National High-tech Development Zone, with a total planned land area of 772.08 mu and a total investment of about 7 billion yuan.

On May 22nd, Huayou Cobalt Co., Ltd. plans to raise an additional 6.25 billion yuan. It will be used for the project with an annual output of 45000 tons of high nickel metal matte, the project of ternary precursor materials for 50, 000 tons of high-nickel power batteries, the construction project of Huayou headquarters Research Institute and supplementary liquidity.

On May 28th, Volkswagen China invested about 1.1 billion / euro to acquire a 26% stake in Guoxuan Hi-Tech and became its major shareholder. On the same day, Guoxuan Hi-Tech disclosed a pre-plan for a non-public offering of A-shares, the total amount of funds raised by the company did not exceed 7.306 billion yuan, of which Volkswagen subscribed to China for a total of not less than 6 billion yuan. According to the plan, the funds raised will be used to include the signed Guoxuan material project with an annual output of 30000 tons of high-nickel ternary cathode materials. In addition, the funds raised will also be used for the industrialization project of high specific energy lithium battery with annual production of 16GWh and supplementary working capital.

6. On September 2, Libao New Materials Company officially supplied goods to Ningde Times. This time, Libao sent 90 tons of M515 products to CATL, which will continue to be supplied in the future. This official delivery marks the substantive stage of the cooperation between Yibin Libao and CATL, and the company will continue to carry out more in-depth and extensive cooperation with CATL.

On October 29th, Rong Bai Technology plans to increase its investment in South Korea's wholly-owned subsidiary JAESE Energy Co., Ltd. with 1.193 billion yuan. (referred to as "JS Co., Ltd."), to build a production and construction project with an annual production capacity of 20,000 tons of high nickel cathode materials in South Korea. Rongbai Technology said that the construction of this high-nickel cathode material project will help the company to open up the Korean ternary cathode material market, enrich the company's overseas sales channels, and improve the company's global strategic layout.

8. On November 17, Fengyuan Co., Ltd. is implementing a high-nickel ternary construction project, which will significantly enhance the company's first-mover advantage in the field of high-performance and high value-added cathode materials. In addition, the company expects to have a production capacity of 25000 tons of cathode materials after the completion of this refinancing project, which will have a strong capacity advantage in the lithium cathode material supply chain industry at home and abroad.

Zhongwei New Materials Co., Ltd. (stock code: 300919), a leading enterprise specializing in the production of lithium materials precursors, officially listed and began trading on the growth Enterprise Market of Shenzhen Stock Exchange.

On December 24th, Xiangtan Electrochemical Technology Co., Ltd. plans to contribute 110.2 million yuan in currency with Xinxiang Zhongtian New Energy Technology Co., Ltd., Jingxi Lisheng Enterprise Management Partnership (limited partnership) (provisional name, subject to the approval of the market supervision and management department), Jingxi Lipeng Enterprise Management Partnership (limited partnership) (provisional name, Subject to the approval of the market supervision and administration department) jointly invest in the establishment of Jingxi Lijin New Materials Co., Ltd. After the establishment of the joint venture company, it is proposed to build a new automatic production line with an annual output of 30,000 tons of lithium manganate, and the project is planned to be carried out in phases, with a capacity of 20,000 tons per year in the first phase, and the annual production capacity will be increased by 10,000 tons in the future depending on the market situation of lithium manganate. the project is currently in the preparatory stage.

On December 29th, the Shanghai Stock Exchange examined and approved the IPO application of Science and Technology Innovation Board of Xiamen Xiamen Tungsten New Energy Materials Co., Ltd. According to the prospectus of Xiamen Tungsten New Energy, 1.5 billion yuan will be raised in this listing, of which 900 million yuan will be used for the industrialization project of 40000 tons of lithium-ion battery materials per year (phase I and II), and 600 million yuan will be used to supplement liquidity.

December 29, Guizhou Zhenhua New Materials Co., Ltd. has completed the listing coaching work, and submitted to Guizhou Securities Regulatory Bureau "CITIC Construction Investment Securities Co., Ltd. on Guizhou Zhenhua New Materials Co., Ltd. initial public offering and listing mentoring work summary materials", applying for counseling acceptance.

SMM battery materials research team

Mei Wangqin 021-51666759

Huo Yuan 021-51666898

Liu Xiaoyi 021-51666716

Yuan Ye 021-51595792